Japan’s Stock Market Surges to Record Highs:

Inside the Tokyo Stock Exchange. Japan’s stock market has recently broken decades-old records, reflecting a major turnaround in corporate and economic performance.

Introduction

Japan’s major stock indices have been hitting historic highs, surpassing levels not seen since the late 1980s bubble era. Both the Nikkei 225 and the TOPIX index have surged to all-time or multi-decade records in 2023–2025, marking a dramatic rebound from the stagnation of previous decades  . Many observers credit policy changes that encouraged Japanese companies to enhance shareholder value, but the underlying driver is Japan’s escape from deflation and robust growth in nominal GDP  . In other words, real economic expansion has combined with corporate reforms to propel the stock market. This carries a clear implication for South Korea’s ambitions: if Korea aims to usher in a “KOSPI 5000” era (with the KOSPI index at 5,000 points), it must complement market reforms with higher economic growth. This report examines how Japan achieved its stock market renaissance and what conditions Korea would need to reach KOSPI 5000, following a comprehensive, in-depth analysis of recent data and policy trends.

Japan’s Lost Decades and Corporate Cash Hoarding

Throughout the 1990s and 2000s, often dubbed Japan’s “Lost Decades,” the country grappled with low growth, deflation, and near-zero interest rates  . The burst of the late-1980s asset bubble led to a prolonged period of economic stagnation. From 1991 to around 2013, Japan’s nominal GDP barely grew at all – by one estimate, nominal GDP in 2013 was roughly the same as in 1991  – and prices were falling, creating a deflationary mindset. In such an environment, Japanese firms became extremely conservative with their finances: many corporations cut investment and hoarded cash instead of pursuing expansion  . By the late 1990s, Japanese companies had shifted from being net borrowers to net savers, meaning they saved more money than they borrowed or invested. This corporate deleveraging was evidenced by firms running financial surpluses (excess funds) year after year.

• Banks and Low Yields: With companies reluctant to borrow and invest, Japan’s banks faced weak loan demand. Households were already net savers, and now corporations were too, leading banks to seek other outlets for funds. As a result, banks increasingly invested in government bonds (rather than riskier business loans or equities). By the early 2000s, a significant share of bank assets was in bonds, helping drive long-term interest rates down to 0% on 10-year government bonds . Interest rates fell to rock-bottom levels in an attempt to stimulate activity, yet the economy remained listless. Notably, stock prices fell alongside interest rates during much of this period, defying the usual pattern where low rates boost equities. The reason was that economic growth and corporate earnings were deteriorating even faster than interest rates were dropping, and Japanese firms paid out very little of their profits as dividends (with payout ratios around only 15–20% in the 1990s). With weak growth and minimal shareholder returns, stocks had little fuel for gains.

• Depressed Valuations: By the early 2010s, Japanese equities had acquired a reputation as a “value trap.” Companies were trading at very low price-to-book and price-to-earnings multiples (many stocks had P/B ratios below 1, meaning the market valued them at less than their book value), reflecting investors’ pessimism. Corporate return on equity (ROE) was chronically low as firms sat on cash and maintained inefficient capital structures. It was common to refer to Japanese companies as having “over-capitalized balance sheets” – lots of cash, little debt, and underutilized assets – which resulted in lackluster returns. This was the backdrop as Japan entered the 2010s: a huge gap between companies’ potential and the meager returns shareholders were actually getting, all against a stagnant economic backdrop.

Turnaround: Shareholder Value Reforms in Japan

Starting in the mid-2010s, Japan initiated a series of shareholder-focused reforms that began to change corporate behavior. These were a part of former Prime Minister Shinzo Abe’s economic agenda and beyond, aimed at shaking up Japan’s corporate culture and improving capital efficiency:

• Stewardship and Governance Codes: In 2014, Japan introduced the Stewardship Code, and in 2015 a new Corporate Governance Code, both designed to encourage better corporate governance and shareholder returns. The Stewardship Code pushed institutional investors (like pension funds and asset managers) to actively engage with companies to boost shareholder value . The Governance Code laid out principles for firms, such as increasing the number of independent outside directors and improving transparency. Together, these policies prodded companies to focus more on return on equity and efficient capital use – a sharp break from the prior norm of hoarding cash “for a rainy day.”

• Focus on Capital Efficiency (PBR < 1 Target): A more direct pressure came from Japan’s stock exchange regulators. In early 2023, the Tokyo Stock Exchange (TSE) sent a clear message: companies with price-to-book ratios (PBR) below 1 must improve or face consequences. In March 2023, the TSE formally requested that listed firms “put more focus on improving capital efficiency,” targeting the many companies whose market value was less than their net assets . At that time, over 40% of companies on the TSE’s Prime section had PBRs under 1 – a situation the exchange saw as unacceptable in a developed market . This push included encouraging firms to unwind cross-shareholdings (where companies mutually hold each other’s shares, a practice that often led to strategic relationships at the expense of shareholder returns) and to deploy their cash stockpiles in more productive ways.

• Surge in Share Buybacks: Faced with these pressures and buoyed by improving profits (as discussed later), Japanese companies responded vigorously through record share buybacks. In FY2024 (year ending March 2024), firms listed on the TOPIX index announced share repurchases totaling approximately ¥18 trillion – an 85% increase from the previous year . According to Ichiyoshi Securities, the total buybacks in calendar 2024 were about ¥18.0 trillion, nearly double 2023’s ¥9.6 trillion . This is the largest amount on record, signaling a sea change in corporate Japan’s attitude toward using cash. By reducing outstanding shares, these buybacks directly boost metrics like earnings per share and also help lift PBRs (since equity gets reduced). Major companies led the way – for example, Toyota Motor announced a massive ¥1.2 trillion buyback program . As Bloomberg noted, Japanese corporations collectively became the biggest buyers of stocks in 2024 via their own buyback programs, which provided substantial support to the market .

• Rising Dividend Payouts: Alongside buybacks, dividends have risen sharply. For decades, Japanese firms’ dividend payout ratios were very low (often in the 20% range of profits). This has changed. In FY2024, the average dividend payout ratio for TOPIX companies reached ~35–36%, up from around 30% a few years prior, and when combined with buybacks, the total shareholder return ratio (dividends + buybacks as a percentage of net income) hit new highs . One analysis noted that Japanese companies’ total payout ratio in 2024 reached about 60% of earnings, on par with European companies and a dramatic rise from prior years . This means a majority of corporate earnings are now being returned to shareholders rather than sitting idle. The shift is so pronounced that it’s reinventing Japan’s image from a “low-dividend, cash-hoarding” market to one where “companies actively share profits with shareholders”.

• Consequences for Lagging Firms: Not all companies have embraced these changes willingly – some needed a proverbial stick. The TSE’s emphasis on capital efficiency came with an implied threat: if a company persistently undervalues itself (PBR < 1 and no plan for improvement), it could be taken private or delisted. This threat has materialized in a wave of takeovers and delistings. 2024 saw almost 100 companies delist from the TSE, the most in a decade . And by the first half of 2025, 59 companies had already delisted or announced plans to – a record pace, on track to exceed the previous year’s total . These departures are often through management buyouts or mergers, sometimes motivated by owners deciding to retreat from public markets rather than face pressure to boost shareholder returns. In other cases, companies pre-empted this outcome by improving their policies – for example, announcing higher dividends or buybacks to avoid being targeted. The overall effect is that being a chronically undervalued company in Japan now has real consequences, adding urgency for management to change their ways .

• Foreign Investor Interest: The corporate reforms and improving shareholder yields have not gone unnoticed globally. After years of international investors being underweight Japan, 2023–2024 saw a strong revival of foreign buying of Japanese equities. In just April 2023, foreigners pumped about ¥5 trillion (≈ $37 billion) into Japanese stocks, a monthly record seldom seen in history . By mid-2023, foreign fund flows into Japan turned decisively positive after several years of outflows . A few high-profile endorsements added fuel: notably, billionaire Warren Buffett publicly praised Japanese stocks (in particular, he increased holdings in Japanese trading companies), which, along with the TSE’s moves, helped spark a re-rating of Japan’s market  . Investors were attracted by cheap valuations combined with clear signs of reform – a potent mix. In fact, by May 2023 the Nikkei’s rally was being attributed to a confluence of “cheap valuations, corporate reforms, money rotating out of China, low interest rates, and optimism from investors like Buffett” . Suddenly, Japan was being viewed as a market with improving governance and strong earnings, yet still relatively undervalued – a compelling opportunity.

Bottom line: Through deliberate policy and investor pressure, Japan has executed a shareholder value revolution. Companies that once prioritized size and market share (with profits as a secondary concern) are now actively buying back shares, raising dividends, and striving to lift ROE. This policy-driven shift in corporate mindset laid crucial groundwork for the stock market’s ascent. However, an equally important piece of the puzzle was macroeconomic – without an improving economy, these corporate moves might not have been enough. Japan’s exit from deflation and return to growth provided the fundamental boost that really allowed share prices to take off.

The End of Deflation: Abenomics and Nominal GDP Growth

While corporate reforms set the stage, the fundamental driver of Japan’s stock surge has been its macroeconomic turnaround – specifically, the end of deflation and a significant rise in nominal GDP. Stock prices in the long run are anchored to corporate earnings, which grow when the economy (and prices) grows. For nearly 20 years, Japan’s economy was essentially flat in nominal terms, but that changed after 2013:

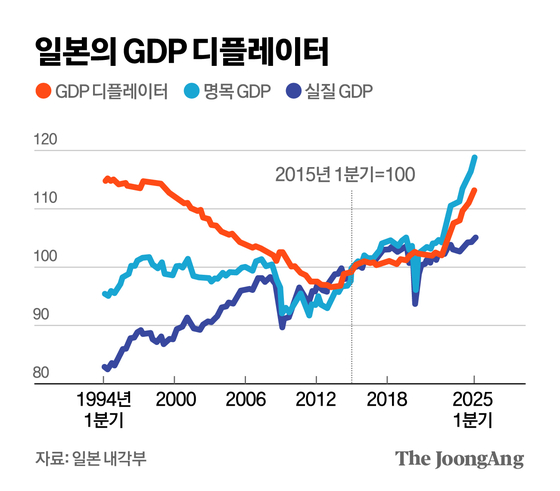

• Deflation and Stagnation (1990s–2000s): Japan’s deflationary era meant that price levels were actually declining for many years. The GDP deflator, a broad measure of prices in the economy, fell steadily. To illustrate, in 1994 the GDP deflator index (2015=100) was around 114, but by 2013 it had fallen to about 96 – a cumulative drop of ~15% in the general price level . In practical terms, this meant that nominal GDP was going nowhere: indeed, from the mid-1990s to early 2010s, Japan’s nominal GDP was basically unchanged (or even shrank slightly) . One stark statistic: between 1995 and 2013, Japan’s nominal GDP declined by over 6% . It’s hard for corporate revenues and profits to grow in such conditions. This explains why, despite zero interest rates and fiscal stimulus, Japan’s stock indexes languished for decades – the denominator (nominal GDP) wasn’t growing. Real economic growth was anemic (averaging ~1% or less in real terms ) and prices were falling, resulting in near-zero nominal growth.

• Abenomics to the Rescue: At the end of 2012, Prime Minister Shinzo Abe launched what came to be known as “Abenomics,” a bold policy package to jolt Japan out of deflation. Abenomics rested on “three arrows” – monetary easing, fiscal stimulus, and structural reforms . The Bank of Japan (BOJ) aggressively expanded the money supply through Quantitative and Qualitative Easing (QQE) starting in 2013, committing to a 2% inflation target . In 2016, the BOJ even introduced a negative interest rate (-0.1%) to further stimulate lending and inflation . On the fiscal side, the government spent heavily at times to support demand. Structural reforms were more gradual, but the overall message was clear: Japan would do whatever it takes to end deflation. A key aspect of this was influencing expectations – convincing businesses and consumers that prices would rise in the future, so it was better to invest and spend now rather than hoard cash.

• Yen Depreciation: Alongside domestic policies, Japan saw a dramatic currency depreciation which helped lift inflation and corporate profits. At the start of Abenomics, the yen traded around ¥80–90 per US dollar. Over the following years, and especially by the early 2020s, the yen weakened significantly. By June 2024, the yen was about ¥160 per USD – roughly half the value of 2012 (the weakest it had been in 37 years) . This was partly a side effect of BOJ easing (as other countries raised rates by 2022–2023, the BOJ did not, making the yen less attractive, and a deliberate outcome of pro-inflation policy). A weaker yen makes Japanese exports more competitive and increases the yen value of overseas earnings for Japan’s many global companies. For example, when Toyota or Sony repatriate profits earned abroad, a weaker yen means those profits translate into more yen. This significantly boosted corporate earnings in yen terms for export-oriented and globally exposed firms, which in turn supported stock prices. The flip side is that the weak yen temporarily caused Japan’s GDP in USD terms to fall (Japan even slipped behind Germany in dollar GDP in 2023 due to the currency effect ), but domestically, what mattered was that nominal GDP in yen was finally climbing.

• Rising Inflation and Nominal GDP: Thanks to these efforts and also helped by a surge in global inflation post-2021, Japan finally escaped deflation. By the late 2010s, inflation was modestly positive (around 0.5–1%), and after 2021, it rose above 2% for the first sustained period in decades . The GDP deflator turned upward after 2013, indicating broad inflation in the economy instead of deflation. Crucially, nominal GDP started to grow at a healthy pace. From the end of 2012 through 2019, Japan’s nominal GDP gained ground (though briefly interrupted by a dip during the 2020 pandemic). Then, with the global inflationary environment of 2021-2022, nominal GDP leapt further. By 2023, Japan’s quarterly nominal GDP was around ¥590–600 trillion (annualized), up roughly 20-25% from a decade earlier . To put it in perspective, Japan’s nominal GDP in 2023 was at a record high in yen terms, finally decisively above the mid-1990s levels. It grew about 23–24% from 2013 to 2023 alone , signaling a clear break from the prior era of stagnation. In the second quarter of 2025, nominal GDP reached ¥633 trillion (seasonally adjusted annual rate)   – another new high. This nominal growth is a combination of real growth (actual increase in output) plus inflation. Even if real growth was modest (Japan’s real GDP growth averaged around 1% in the 2010s), the addition of 1-2% inflation on top made a big difference in nominal terms.

• Corporate Earnings Rebound: With prices and nominal GDP rising, Japanese companies saw a strong rebound in revenues and profits. Many large firms achieved record profit levels in recent years, aided by the weak yen and improved domestic demand. A Reuters analysis noted that in 2023 a “strong earnings season, a weaker yen, and an economy showing signs of sustained recovery” helped fuel the Nikkei’s rise . In other words, it wasn’t just hype – companies were delivering better results. By shedding the deflationary malaise, Japan unlocked growth in top-line sales that had been elusive for years. This improvement in fundamental performance provided the fuel for stocks to rally once the spark of reforms and investor interest was applied.

To summarize, Japan’s return to nominal GDP growth was the essential foundation for its stock market to reach new heights. Corporate governance changes created a more favorable distribution of profits to shareholders, but there needed to be profits in the first place. Once deflation ended and nominal GDP rose, the rising tide lifted corporate earnings across the board. This combination of micro reforms and macro growth is what allowed the Nikkei 225 to finally break a 33-year-old record. As we will see next, the data bear out a strong correlation between Japan’s stock index and its nominal GDP, reinforcing the point that economic growth (especially nominal growth) is a critical ingredient for stock market success.

Nominal GDP as a Driver of Stock Market Highs

Japan’s experience underscores a fundamental relationship: stock prices and nominal GDP tend to move in tandem over the long run. When the economy (in nominal terms) is expanding strongly, corporate revenues and profits generally grow, pushing stock indexes higher; when nominal GDP stagnates, corporate earnings stagnate, and stock indexes flounder. In Japan’s case, this correlation has been striking:

• Statistical Correlation: Analysts often point out the high correlation between the Nikkei 225 index and Japan’s nominal GDP over the decades. By one analysis, the correlation coefficient between Nikkei levels and nominal GDP was about 0.87 (from 1994 to 2025) – an exceptionally high positive correlation【User†(as cited in the prompt)】. This means they tend to rise and fall together. The intuition is straightforward: the Nikkei is essentially a proxy for the aggregate market value of major Japanese companies. That aggregate value will grow if companies’ earnings prospects improve – which they do when the overall economy (especially nominal GDP) is growing. During the “Lost Decades,” nominal GDP was flat and the Nikkei was a fraction of its 1989 peak. Once nominal GDP started rising in the 2010s, the Nikkei began a sustained climb.

• Nikkei and TOPIX Reach Record Highs: The effect of the reforms + GDP growth combo can be clearly seen in market milestones. In June 2023, the Nikkei 225 crossed the 33,000 mark, hitting its highest level since March 1990 – a 33-year high . By late 2023 and into 2024, it hovered in the mid-30,000s, closing in on its 1989 bubble-era peak (38,915). The broader TOPIX index (which covers all TSE Prime market stocks) actually surpassed its historical peak (from 1989) during 2023, as many previously laggard companies’ stocks finally rose. Then, in 2023-2025, as corporate buybacks and foreign inflows accelerated, the Nikkei pushed even higher. In 2023, the Nikkei gained about 20% , making it one of the best-performing major indices globally that year. Fast forward to September 2025: the Nikkei broke through 45,000 points for the first time ever  , well beyond its late-80s high. In other words, the Nikkei finally achieved a true all-time high in nominal terms, not just a “since 1990” high. For a market that languished below half its bubble peak for decades, this is a remarkable turnaround. It underscores how unusual and powerful the current rally has been – and it coincided with Japan’s nominal GDP also reaching unprecedented levels.

• Key Drivers of the Rally: Why did investors bid up Japanese stocks to such heights? We’ve partly answered this: surging corporate earnings and massive shareholder payouts played a role. A weaker yen, as mentioned, boosted export-sector earnings. Domestically, consumer prices began rising, and unemployment stayed low, supporting consumer spending – so many sectors saw improvements. In 2023, Japan’s economy was notably resilient even as other countries slowed, and this fed into earnings optimism . Meanwhile, the corporate governance story – higher ROE, more buybacks – signaled that these earnings would translate into greater returns for investors rather than sitting idle. As a result, investor sentiment on Japan flipped from skepticism to enthusiasm. Foreign funds that had avoided Japan rushed back in (over $30 billion of foreign net buying flowed in during the first half of 2023 alone) . As one Japan-based portfolio manager described, “Japan is suddenly attracting a lot of interest, as it hits its highest market level since the Bubble” . This shift was amplified by global factors: some investors rotated out of China (due to geopolitical and growth concerns) into Japan, seeing it as a comparatively stable and improving story .

• ROE and Valuation Improvement: A core outcome of the reforms was a rise in Return on Equity (ROE) across corporate Japan. For decades, Japan’s average ROE was in the single digits, far below Western counterparts. But with companies buying back stock and focusing on profit margins, ROEs have been climbing. Higher ROE generally justifies higher price-to-book ratios, so stock valuations rose accordingly. By 2024, Japan’s market overall was re-rated upward – yet still not excessively so. Even after the rally, Japanese stocks were valued at around 13–15 times forward earnings and about 1.3 times book value on average, which was cheaper than U.S. stocks (S&P 500 at ~20+ times earnings)  . This meant investors still saw room for upside, especially if earnings continued to grow. In fact, the market capitalization of Japanese stocks as a percentage of GDP rose to about 163% of GDP in 2024 (up from 146% in 2023) , indicating that stock values were growing much faster than the economy – a sign of both real growth and improved investor appetite.

• Yen and Stock Relationship: It’s worth noting another correlation: the inverse correlation between the yen’s strength and the stock market. Historically, a weaker yen tends to lift the Nikkei (since so many Japanese companies are exporters). From 1994 to 2025, the Nikkei and the USD/JPY exchange rate showed a moderately high correlation (around 0.66)  – meaning as the yen fell (higher USD/JPY), stocks rose. This held true in the recent rally: the yen’s decline to multi-decade lows was another tailwind for stocks. However, fundamentally, it all ties back to earnings and GDP: a weaker yen was one mechanism that helped boost nominal GDP (via export revenue and imported inflation), again feeding the main engine.

In summary, Japan’s stock market boom has been underpinned by genuine economic growth and profitability improvements. It’s a textbook case where nominal GDP growth (finally achieved after years of policy efforts) translated into higher corporate earnings, which combined with shareholder-friendly reforms, translated into higher stock prices. The lesson for other markets, like Korea’s, is that if you want to see a major, sustained stock index increase, you need the fundamental earnings base to grow – which ultimately comes from a growing economy. Financial engineering (like higher dividends or buybacks) can unlock value, but only to a point; beyond that, the size of the economy and corporate sector must itself expand. Japan managed to do both, hence the historic highs in its stock indices.

Korea’s Quest for ‘KOSPI 5000’: Policies to Unlock Market Potential

South Korea has been closely observing Japan’s playbook as it contemplates how to elevate its own stock market. Korea’s benchmark KOSPI index (representing the Seoul stock exchange’s main board) has long been regarded as undervalued relative to Korea’s economic size and corporate earnings potential – a phenomenon often termed the “Korea Discount.” Despite being the world’s 10th largest economy, South Korea’s market valuation metrics (P/E, P/B ratios) have lagged global peers . Several structural issues have contributed to this discount:

• Historically low dividend payouts by Korean companies (which typically reinvested or held cash rather than returning it to shareholders).

• Conglomerate (chaebol) governance issues, including complex ownership structures and occasional minority shareholder neglect, which created a perception of risk or unfairness.

• Repeated market scandals and unfair trading incidents (e.g. incidents of stock price manipulation or insider trading) that eroded investor trust over time.

• Regulatory and tax policies that sometimes disincentivized stock investments (for instance, plans to broaden capital gains taxes for retail investors, which were viewed unfavorably by the market).

Recognizing these issues, Korean policymakers and politicians have rolled out an agenda to improve the capital market’s attractiveness and aim for a significantly higher KOSPI level – specifically, targeting 5,000 points (for context, the KOSPI’s all-time high so far was about 3,300 in mid-2021, and it traded around the 2,500–3,200 range in 2023-2024). In 2025, the main opposition party (Democratic Party, DP) even established a dedicated “KOSPI 5000 Special Committee” to push reforms that could help achieve this goal . The committee’s formation underscores how reaching KOSPI 5000 has become a prominent policy discussion, seen not just as a market goal but as a way to “unlock a Korea Premium” instead of a discount .

Key reform initiatives and proposals in Korea include:

1. Amendments to the Commercial Act (Corporate Law): One major legislative focus is altering corporate governance rules via the Commercial Act. Proposed changes (some of which have passed in 2023–2025) aim to strengthen minority shareholder rights and board independence  . For example:

• Broadening the fiduciary duty of directors to explicitly require acting in the interest of shareholders (not just the company or controlling stakeholder). This is to make directors more accountable to investor interests .

• Introducing cumulative voting and separate election of audit committee members so that minority shareholders have a better chance to influence board composition and oversight . (Under cumulative voting, shareholders can concentrate votes on specific candidates, helping minority blocs elect a director; separate audit elections prevent controlling shareholders from having total say over who monitors management.)

• Making it easier to bring class-action suits or hold executives responsible for misconduct, thereby tightening director liability and encouraging more transparency.

These changes echo some of Japan’s governance improvements, though going further in some respects. In fact, a revised Commercial Act incorporating some of these ideas passed the National Assembly in July 2025 with bipartisan support . The new law, among other things, allows minority shareholders to have a stronger voice and curtails certain powers of dominant shareholders in appointing auditors. This legal update was followed by a noticeable positive reaction in the stock market, suggesting investors welcomed the reforms . The DP’s special committee has signaled even more robust revisions in the pipeline (such as potentially mandating a certain percentage of independent directors, etc.), with the belief that these will boost investor confidence and thus stock valuations .

2. Capital Market and Regulatory Reforms: Another area is improving market fairness and transparency. Korean regulators have been working on:

• Tougher enforcement against insider trading and market manipulation. After several high-profile stock manipulation scandals (for instance, a notorious incident in 2022-2023 involving coordinated manipulation of certain small-cap stocks), there is momentum to implement a “one strike out” policy where anyone caught in serious market fraud faces a lifetime ban or harsh penalties【User text】. The idea is to deter would-be manipulators and reassure investors that Korea’s markets are clean. The KRX (Korea Exchange) and Financial Supervisory Service have stepped up real-time monitoring of trading as well .

• Modernizing disclosure rules. This includes requiring more timely and detailed public disclosures from companies, adopting global best practices so that investors have fuller information. There is also talk of English-language disclosures for major firms to attract foreign investors.

• Market infrastructure upgrades. For example, simplifying procedures for foreign investors, and perhaps adjusting short-selling regulations (Korea has had on-and-off bans and limits on short selling, which some argue deter foreign participation). The goal is a more investor-friendly market that can integrate into global capital flows smoothly.

3. Tax Policy Changes: The government and lawmakers have eyed tax reforms to encourage stock investment and shareholder returns:

• Dividend Taxation: One proposal is to treat dividend income separately (and potentially more leniently) in taxation for individual investors【User text】. By making dividends taxed at a flat, possibly lower rate (separate from general income), investors would be more inclined to seek dividend-paying stocks, and companies would be more inclined to pay them. This mirrors practices in some countries where dividends have preferential tax treatment to avoid double taxation.

• Incentives for Share Cancellation: Korean companies often hold substantial treasury shares (stocks of themselves that they’ve bought back but not canceled). These can be reissued, so the market often doesn’t treat buybacks as permanently reducing supply unless shares are canceled. Policymakers are considering mandating or incentivizing the cancellation of treasury shares  after buybacks, which would permanently boost existing shareholders’ proportional ownership. Essentially, they want firms to actually retire the shares they repurchase, to more definitively increase shareholder value and prevent companies from hoarding treasury stock as “war chests” to deter takeovers.

• Capital Gains Tax Threshold: Korea has had rules that classify investors holding over a certain amount in one stock as “large shareholders” who then incur capital gains taxes on stock sales (whereas smaller investors were exempt). At one point, there was a plan to drastically lower this threshold (to bring more people into the tax net), but that was viewed as potentially depressing stock investment. In 2023, the government decided to keep the threshold at the higher level (₩10 billion or ₩50 billion in holdings, depending on context) rather than lowering it【User text】. This means the vast majority of retail investors remain exempt from capital gains tax on stocks, which is a pro-market stance. Additionally, a proposed comprehensive financial investment income tax (that would tax overall portfolio gains) was deferred. These moves ensure that investing in stocks remains tax-advantaged for most people, aiming to encourage greater public participation in the market.

4. Investor Trust and Market Culture: Beyond rules and numbers, there’s an emphasis on changing the market culture in Korea to favor equity investment and trust in markets. This involves:

• Crackdown on Past Scandals: The government has promised thorough investigations and punishment for past stock manipulation rings and corporate accounting frauds. By visibly addressing these, they hope to turn the page and show that such behavior will not be tolerated going forward .

• Encouraging Equity Investment: South Korean households have traditionally favored real estate and bank savings over equities. Policymakers talk about channeling some of the massive liquidity in property and cash into the stock market. One statistic: as of early 2023, the total financial assets of Korean households, companies, and government was ₩1,253 trillion (₩1.253 quadrillion, or about $1.05 trillion)【User text】. Even a fraction of that moving into stocks could fuel a big rally. By improving market confidence, they hope more of the public will invest in equities (either directly or via funds/pensions), providing a domestic bid that can support higher valuations.

• “Korea Premium” Vision: The ultimate aim is to shed the “Korea Discount” label and achieve a “Korea Premium.” This means Korea would be viewed as a place with exemplary corporate governance and vibrant capital markets, possibly even commanding higher valuations than global averages due to its tech-savvy economy and growth potential . It’s an ambitious vision, essentially to have KOSPI 5000 as a symbol that Korea’s market is valued commensurately with its economic rank.

These efforts have already had some impact. By mid-2025, the KOSPI was trading in the low 3,000s (it crossed 3,200 in July 2025) , which is higher than it had been in a couple of years. Part of this rise was attributed to anticipation and realization of reform measures – much like how Japan’s market reacted positively to governance changes. Notably, when the Commercial Act amendment passed in early July 2025 to improve shareholder rights, the KOSPI jumped in relief, indicating investors prize such reforms . Korean lawmakers and officials often pointed out that Japan’s Nikkei soared to record highs after implementing shareholder-friendly policies, so Korea could do the same. Indeed, Korea’s initiatives like encouraging share cancellations and raising dividend payouts are explicitly inspired by Japan’s success.

However, a critical question remains: Even with all these market-friendly changes, can the KOSPI reach 5,000 without stronger economic growth? Korea’s reforms, like Japan’s, can help unlock value and raise valuations to some extent, but the size of the stock market ultimately reflects the size of the economy and corporate earnings. In the next section, we will analyze Korea’s growth outlook relative to the KOSPI 5000 goal, and why many experts argue that “KOSPI 5000” will require a significant boost in Korea’s GDP growth rate – a parallel to how Japan’s stock boom needed Japan’s GDP to start growing robustly again.

The Growth Imperative: Why GDP Matters for KOSPI’s Ascent

While market reforms are necessary for improving valuations, they may not be sufficient to hit the KOSPI 5000 target unless accompanied by stronger economic growth. The reasoning is straightforward: stock prices, in aggregate, are ultimately a reflection of corporate profits, which in turn depend on the overall economy’s size and growth rate. If Korea’s economy grows slowly, corporate earnings will likely grow slowly, putting a natural brake on how far the stock index can rise even if valuation multiples increase. Let’s break down the considerations:

• Historical Growth vs. Stock Returns: Korea’s own history shows a parallel between nominal GDP growth and the KOSPI’s performance. From 2000 to 2024, Korea’s nominal GDP grew at an annual average of ~5.9%, while the KOSPI’s annual return averaged about 6.7%【User text】. The numbers are in the same ballpark, indicating that over the long run, the stock index did only slightly better than nominal GDP, likely due to some valuation changes and dividends. This makes sense: over decades, one would expect stock market growth (including reinvested dividends) to roughly track nominal economic growth plus maybe a small premium. Crucially, if nominal GDP growth slows, it’s likely the stock market’s growth will also slow, unless valuations dramatically re-rate upward (which has limits).

• Current Growth Outlook: South Korea’s economy, like Japan’s, has matured and is facing demographic headwinds (aging population, low birth rates) as well as productivity challenges. The country’s potential GDP growth has been on a declining trend. In the 2000s it was often cited around 4-5%, in the 2010s around 3%, and by the mid-2020s some estimates put Korea’s potential growth below 2%. A Korean editorial even noted that potential growth is “well under 1 percent” now  – which might be a pessimistic take, but it captures the concern that trend growth is low. The Bank of Korea’s more official estimates still suggest around 2% or a bit below in the mid-2020s for potential real growth, but that’s far below the roaring decades of the past. If we add an inflation target of ~2%, that implies nominal GDP might grow around 3-4% annually under current conditions. Indeed, a prominent economist in Korea (like the author of the article provided) projected Korea’s nominal GDP growth in the next 5 years to be about 3.8% per year (comprising ~1.8% real growth and ~2.0% inflation). At ~4% nominal growth, what can we expect for the KOSPI? Likely on the order of 4–5% annual increase (assuming valuations don’t change drastically). An annual 5% stock rise for five years would only yield roughly a 27% total increase, which from a base of around 3,000 would reach only ~3,800 on the KOSPI【User text】. That’s far shy of 5,000. In other words, if the economy plods along, so will the stock index, regardless of reforms.

• The Need for Higher Growth: To realistically achieve KOSPI = 5000 in, say, the next 5–10 years, Korea would either need (a) a major valuation re-rating (i.e., global investors suddenly assigning much higher multiples to Korean stocks), or (b) a significant acceleration in nominal GDP growth, or ideally both. The valuation re-rating is happening to an extent due to reforms, but it has its natural ceiling – if Korea’s P/E ratios approach, say, 15–18x (up from perhaps ~10–12x historically), that’s a big improvement but not enough alone to go from 3000 to 5000 on the index. Thus, attention turns to growth. Korea’s government is aware of this: the current administration under President Yoon (a conservative government) has emphasized policies for “dynamic innovation-led growth”, and the opposition (DP) also ties KOSPI 5000 to boosting growth. There is talk of lifting Korea’s potential growth back up to 3% through structural reforms such as labor market changes, deregulation, and fostering new industries【User text】. If such efforts bear fruit and real growth could sustainably rise to ~3% (from ~2% or less now), and if inflation is around 2%, then nominal GDP could grow ~5% a year. At 5% nominal growth, the KOSPI could feasibly rise ~7-8% per year (if some leverage effect or slight multiple expansion), which compounded over, say, 5-7 years could approach the 5000 mark. Essentially, Korea likely needs at least mid-single-digit nominal GDP growth to have a shot at KOSPI 5000 in the medium term. This means reigniting engines of growth – be it technology innovation, productivity improvements, or even population boosts (through immigration or higher birthrate, which is a very tough issue in Korea) – becomes part of the stock market strategy.

• Quality of Growth Matters: It’s not just the percentage growth, but where growth comes from. For stock market prosperity, growth driven by thriving industries and corporate innovation is key. If GDP grows via, say, government spending or housing booms, it might not translate into corporate profit growth equally. The JoongAng Ilbo (Korean newspaper) pointed out that for the stock rally to be meaningful, capital should shift into “industries generating innovation and productivity” – in other words, Korea needs its tech sector, green industries, bio-health, etc., to drive growth and excite investors . Currently, some critics note that the mini-rally in 2023-2025 was led by financial and construction stocks (which jumped on legal changes and housing market movements) rather than new economy stocks . For a sustained run to 5000, Korea would want to see its Samsungs, SK Hynixes, bio-tech firms, EV battery makers, and other globally competitive companies deliver strong growth that lifts the whole index. One encouraging factor: Korean companies are global players in semiconductors, EV batteries, shipbuilding, etc. If global demand in those areas is robust (and not overly hindered by geopolitical issues), it could support Korea’s growth narrative.

• Risks of Overreach: Some analysts caution Seoul’s policymakers not to become too fixated on the stock index number in isolation. An op-ed titled “Rushing toward KOSPI 5000 puts the cart before the horse” argued that artificially pushing stock prices (through pressure on companies to pay out more, for example) without ensuring the real economy is improving could be dangerous . Share prices should reflect economic reality, and while wealth effects from higher stocks are nice, they’re not a substitute for genuine economic momentum . The op-ed drew parallels to policy mistakes where form is prioritized over substance. For instance, if companies are forced to spend cash on buybacks/dividends but in doing so they neglect investment in R&D or expansion, it could undermine long-term growth – which eventually circles back to hurt the stock market. The lesson is that policy should enable and accompany real growth, not replace it. In Korea’s context, this means alongside corporate governance reform, there must be structural economic reforms: improved labor productivity, encouragement of startups, perhaps regulatory easing in sectors like fintech or biotech, and so on. Only by improving the fundamentals will KOSPI 5000 not only be reached but be sustainable.

• Global Environment: We should also acknowledge external factors. Korea, being an export-driven economy, depends on the global economic climate. Japan’s stock surge coincided with a benign global environment (at least until 2022, when inflation globally caused some strains, but Japan’s unique policy stance insulated it somewhat). For Korea, factors like U.S.-China relations, global trade demand, and worldwide monetary policy will influence its market. A global bull market or ample global liquidity would help KOSPI 5000, whereas global recessions or financial crises would obviously hurt the prospects. Thus, Korea’s path to 5000 is not entirely within its control. Nonetheless, the country’s focus rightly is on what is within its control: domestic policies that make the market and economy more vibrant.

In essence, to get to KOSPI 5000, Korea must create the conditions for higher corporate earnings – and that means higher growth. Market reforms can help unlock value (perhaps taking KOSPI from, say, 2500 to 3000+ just by improving P/E ratios), but to go beyond and add several trillions of dollars in market cap up to 5000, there needs to be more profit for investors to pay for. As one Korean financial executive remarked, the recent rally felt like just correcting undervaluation, “but that by itself won’t sustain a rally. Capital must flow into industries leading growth and innovation.”  True words that mirror the Japanese experience: Japan only truly broke out when innovation and expansion (even modest) returned alongside inflation. Korea will likely need a similar genuine growth narrative – whether it’s technological breakthroughs, new markets, or productivity leaps – to propel its stock index to that aspirational 5,000 level.

Conclusion

Japan’s stock market resurgence provides a powerful case study in how combining structural reforms with macroeconomic growth can create a virtuous cycle for equities. After decades of stagnation, Japan took deliberate steps to improve corporate governance and capital efficiency – from stewardship codes to pushing companies on shareholder returns. These measures unlocked value and made Japanese equities more attractive, setting the stage for a market rally. But the rally truly gathered steam only when Japan simultaneously escaped deflation and achieved robust nominal GDP growth. With rising inflation and a weaker yen boosting profits, Japanese companies saw earnings climb and had both the motive and means to reward shareholders, leading the Nikkei 225 and TOPIX to soar to record highs  . In short, policy reforms lit the fuse, but economic growth provided the powder. The result: a stock market reaching levels once thought unimaginable after the long slump.

Korea is now attempting a similar feat – and the lessons from Japan are instructive. Korea’s reforms to enhance shareholder rights, increase transparency, and demand better payouts are likely to improve the “Korea Discount” and could lift the KOSPI higher in the near term. Indeed, we have seen Korean stocks respond positively to governance changes and the prospect of more investor-friendly policies. However, the experience of Japan (and economic common sense) shows that without stronger underlying growth, there is a ceiling to stock market gains. Korea’s aspiration for a KOSPI 5000 will test whether the country can reinvigorate its growth engine at a time when its population is aging and productivity growth has slowed. It will require structural changes and innovation – essentially a Korean version of boosting nominal GDP in a sustained way.

The good news is that Korea has considerable strengths – a highly educated workforce, world-leading companies in tech and manufacturing, and a capacity for rapid innovation (as seen in its rise in industries like semiconductors, smartphones, electric vehicle batteries, and the cultural sector with the Korean Wave). If these strengths can be channeled into a new wave of growth (perhaps via digital transformation, AI, green technology, etc.), then corporate earnings will follow, and so will the stock index. Stock market value, after all, can expand dramatically when fueled by genuine economic dynamism. As an illustration, one Korean commentary noted that if KOSPI 5000 were achieved, the total market cap of Korean stocks would be around ₩4 quadrillion (about $3 trillion) – which sounds huge, but then pointed out that a single U.S. company (Nvidia, the AI chip giant) now has a market cap well over $1 trillion, proving that explosive growth stories can create immense value  . In other words, with the right growth drivers, what seems ambitious is not impossible.

In conclusion, “real” growth is the key to a “real” KOSPI 5000 era. Japan taught us that elevating a stock market to new heights is not achieved by financial engineering or policy alone; it must ride on the back of rising national income and corporate prosperity. Korea’s journey to 5000 will thus depend on executing a dual strategy: continue the market reforms to ensure investor confidence and fair valuation, and concurrently unleash policies that drive economic growth and innovation. If both tracks are pursued successfully, Korea can not only reach KOSPI 5000 but sustain it, turning the Korea Discount into a Korea Premium. If one track falters – especially the growth track – then KOSPI 5000 might remain elusive or short-lived. The stakes are high, but the blueprint is there: combine pro-market reforms with pro-growth policies, and a nation’s stock market can climb to unprecedented peaks, as Japan’s remarkable resurgence has demonstrated.

Sources: Recent analysis and data from Japan’s markets  , economic statistics from official releases , and commentary from Korean financial experts and media   have been used to support this deep-dive assessment. The evidence consistently highlights the interplay of policy, corporate behavior, and macroeconomic trends in determining the trajectory of stock indices. Both Japan and Korea’s cases reiterate that robust economic growth is indispensable for achieving and sustaining stock market milestones like new record highs or ambitious index targets  .

'경제와 산업' 카테고리의 다른 글

| 국내 외국인 노동자 현황과 최근 추이 (0) | 2025.10.06 |

|---|---|

| HBM 시장 점유율 하이닉스 마이크론 삼성전자 (0) | 2025.09.24 |

| US–Korea Tariff Negotiation Citation of Doctrine of the Mean chinese philosophy (0) | 2025.09.19 |

| 관세협상 김정관 장관의 중국철학 ‘중용’ 인용 트럼프 러트닉 (0) | 2025.09.19 |

| 미국과 무제한 통화스와프를 체결한 국가와 중앙은행 (0) | 2025.09.16 |